Global Emerging Markets

Burgeoning Economies

The Emerging Markets refer to the world's largest burgeoning 'investable' countries, including China, India and most countries in the rest of Asia, eastern Europe, Africa and Latin America. Home to over 80% of the world’s population it is incredibly diverse - in its people, politics and economic development – offering investors a rich source of opportunity.

Broadly, the Emerging Markets exhibit pent-up demand for industrial and consumer goods. There are periods of over- and under-investment that impact profitability, as with all markets, but there is nevertheless underlying growth as affordability improves. Eventually, a virtuous cycle of domestic savings, investment, education, innovation and consumption takes hold, unveiling a long runway for technology and productivity.

Demand evidently accelerates once sufficient income allows affordability to flourish: a tipping point from around USD 2,000 real GDP per capita. Rapid economic development has permanently reshaped the world economy over recent decades, with Emerging Markets now dominating the share of the world population having attained a level of income above this tipping point.

Attractive investment opportunities, however, also require “scarcity”. Scarcity is to either differentiate (via product, price or location) or to produce with lower cost, and to prevent abundant supply of competitors’ otherwise substitutable products. This matters greatly in Emerging Markets where attractive demand growth is evident to many competitors. The apparent paradox of poor equity returns from some stocks in high GDP growth emerging economies is not in fact a paradox at all. Demand is not lacking, instead a lack of adequate profitability from excessive competition (supply) is the key stock driver. China’s industrial engine for example has produced lots of everything and benefitted global consumers with low prices, but individual companies’ equity holders have benefitted only where supply conditions have permitted.

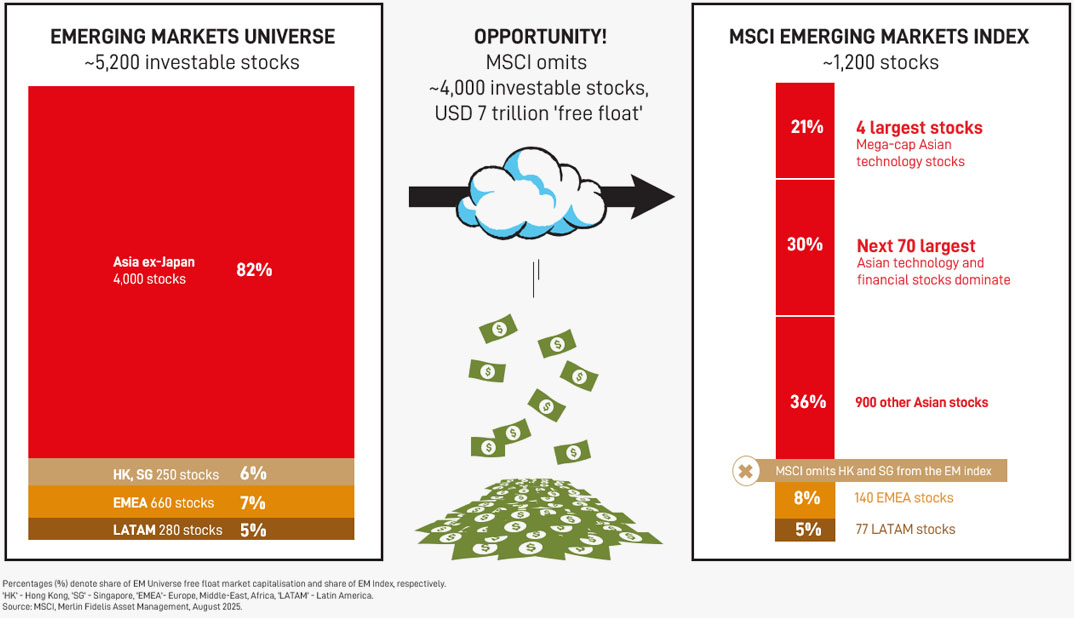

The diversity of companies in the Emerging Markets universe will inevitably comprise stocks with contrasting fundamentals and their mispricing – ideal conditions for active management! Meanwhile the index which attracts passive investment flows is heavily biased to very large companies and a few cyclical sectors (see below).

The Case for Active Management

Performance is measured against the MSCI benchmark1, which is replicated by readily available low-cost index funds. Although it includes roughly 1,200 stocks, it is heavily skewed to a handful of large Asian technology companies and to cyclical sectors; just 4 Asian technology companies make up over 20% of the index, while the cyclical technology, financial and resources sectors2 make up over 70%. That compares to a rich opportunity set3, particularly for long-term institutional capital, of over 5,000 stocks. Active investors can avoid the large index positions when risks are unacceptably high, or when superior prospective returns are available elsewhere, and instead choose from the many alternative investment payoffs available.

¹ MSCI Emerging Markets Net Index USD (ticker NDUEEGF)² GICS sectors have been adjusted to be more indicative, for example several large Consumer Discretionary stocks are actually Technology stocks

³ Roughly 5,200 stocks with >USD1 billion market capitalisation, including Hong Kong and Singapore